The State of Startups report, published annually by Carta, is currently the best quantitative portrait of the global venture capital game.

Even though it is a report focused on data from North American companies, the incentives analyzed, such as dilution, risk, scale, liquidity, and return, are universal and work the same way in any geography.

After an in-depth reading of the material, I bring 7 insights for founders and investors who want to start 2026 with a better understanding of our market.

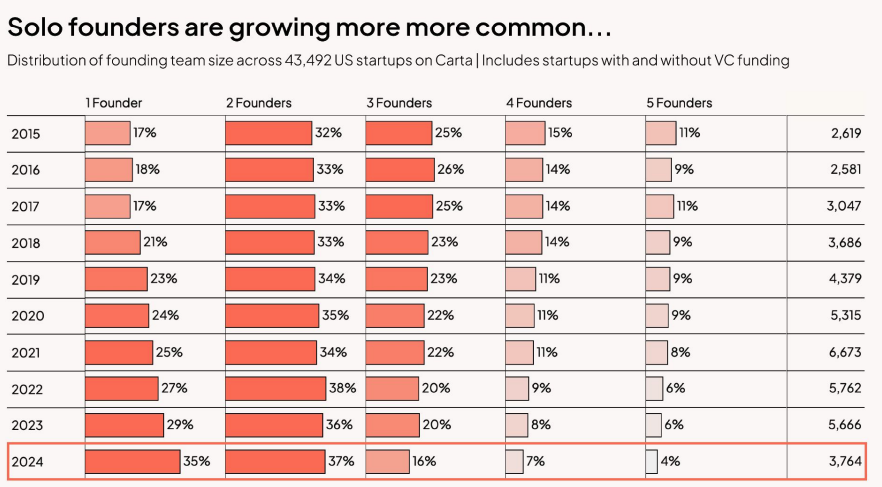

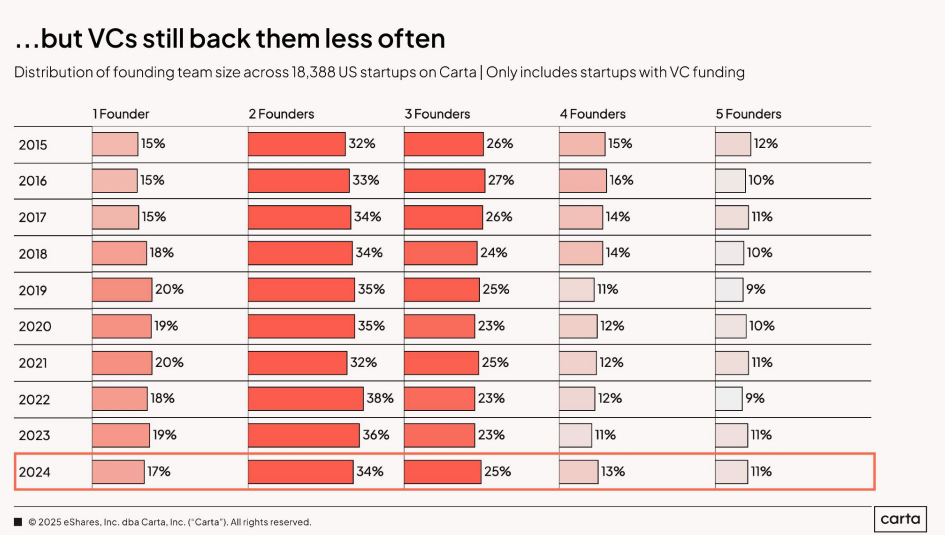

1. The Rise of Solo Founders

The percentage of solo founders doubled in 10 years, from 17% to 35%. During the same period, the share of startups with a single founder that raised money from VC grew very little, from 15% to 17%.

These data show that, even with the increase in the number of solo founders, VCs continue to prefer companies led by teams with two partners or more. Not because of conservatism, but because of risk asymmetry. Building something great is already difficult as a team. Alone, the emotional and execution risk increases greatly.

Much of this trend comes from the wave of MicroSaaS + AI: individual entrepreneurs creating products with very low marginal costs, without the ambition to build venture-scale companies. They are efficient businesses, often excellent, but in practice, lifestyle businesses.

Solo founders are working better and better for small businesses. For venture-scale, startups with a single founder, on average, remain a structurally weaker bet.

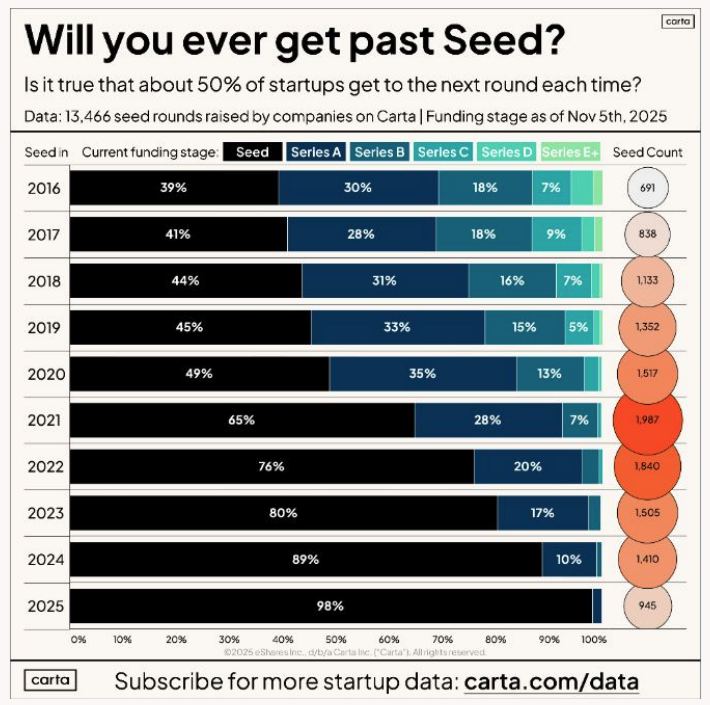

2. The game is (still) difficult

Another conclusion from the report is clear: the growth game for startups remains tough. The Seed graduation rate for Series B, in the oldest U.S. vintages, is around 15%. In Brazil, estimates from the District and Sling Hub point to somewhere between 3% and 9%.

In other words, capturing a round doesn't solve the problem, it just buys time. And with each rung, the bar goes up.

Founders who make it far along the journey (post-Series D) end up, on average, with 12% equity. But there is a large variance, which is directly related to capital efficiency. Very disciplined founders, for example, manage to hold up to 26% of participation in that same stage.

Venture is that. Raise outside capital to buy time and try to create something big fast enough. When it works out, the return is enormous for everyone involved, including the founders. After all, 12% of US$ 1 billion over 8 to 10 years is a lot of money.

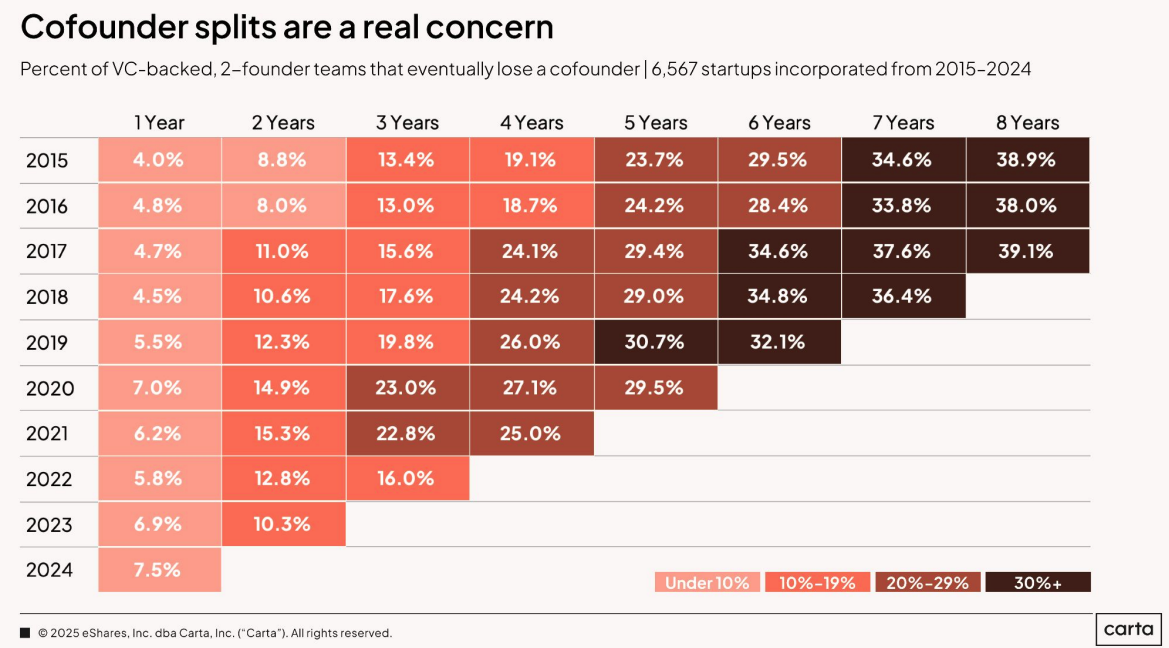

3. Think about the breakup from day zero

According to the report, after 5 years of founding, there is a 30% chance that the company will lose at least one co-founder. That probability rises to 40% in 8 years. In teams of three or four founders, some kind of separation is almost certain. And if this is poorly planned or structured it can be very costly. Or even cost the company itself.

Because of this, we recommend adding renewed vesting every round, even if partially. It seems hard for us to ask for this as investors, but it helps preserve the company. If someone leaves, for whatever reason, it doesn't become a burden. The company needs this equity to attract new key people and attract new rounds.

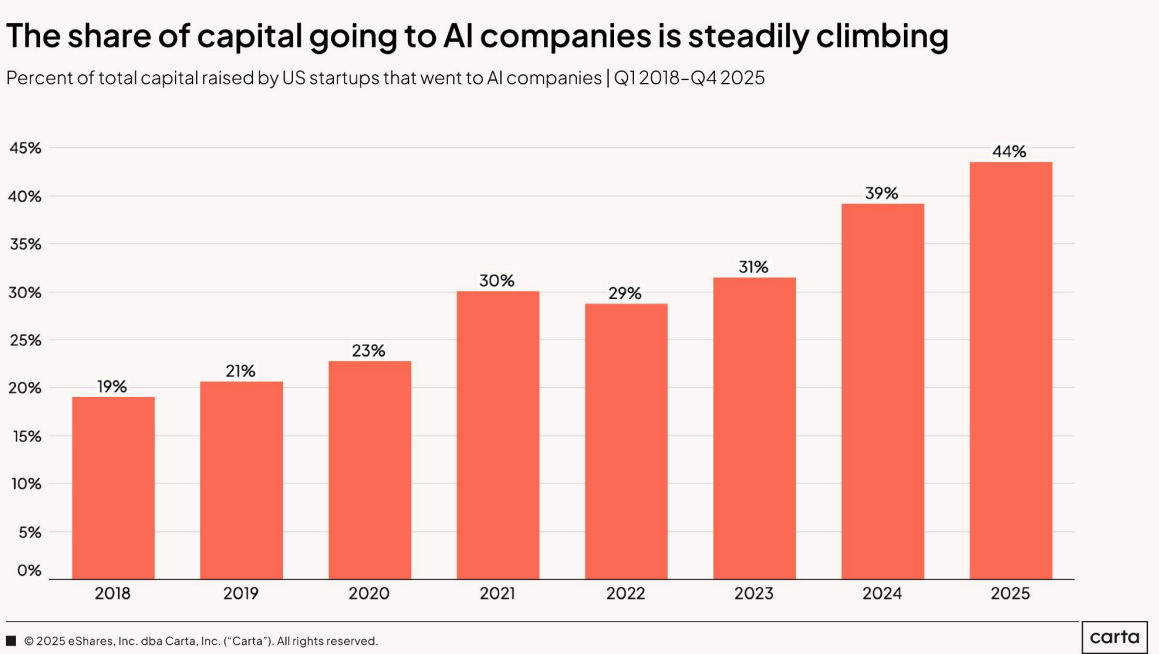

4. AI dominance grows

Almost half of the funding in 2025 (44%) was earmarked for AI companies. In the USA, that's all they talk about, and in Brazil, it's not much different. Of course the Mega Rounds — rounds worth over US$ 100 million — represent about 15% of this, but it's still a very relevant number.

With a greater volume of investment directed to AI, an incentive is created for the creation and development of businesses focused on this technology. And we're already seeing that happening here in Brazil. To give you an idea, in our DealFlow currently, more than 1/3 of companies are already born with AI in Core.

However, having AI in the name or in the business plan is not enough to attract the attention of investors. To do this, it is necessary to demonstrate that the company, in fact, uses technology to create a defensible barrier to entry and is not just a Wrapper of foundational models.

In short: to attract attention, it's not enough to have AI but to be, in fact, an AI company.

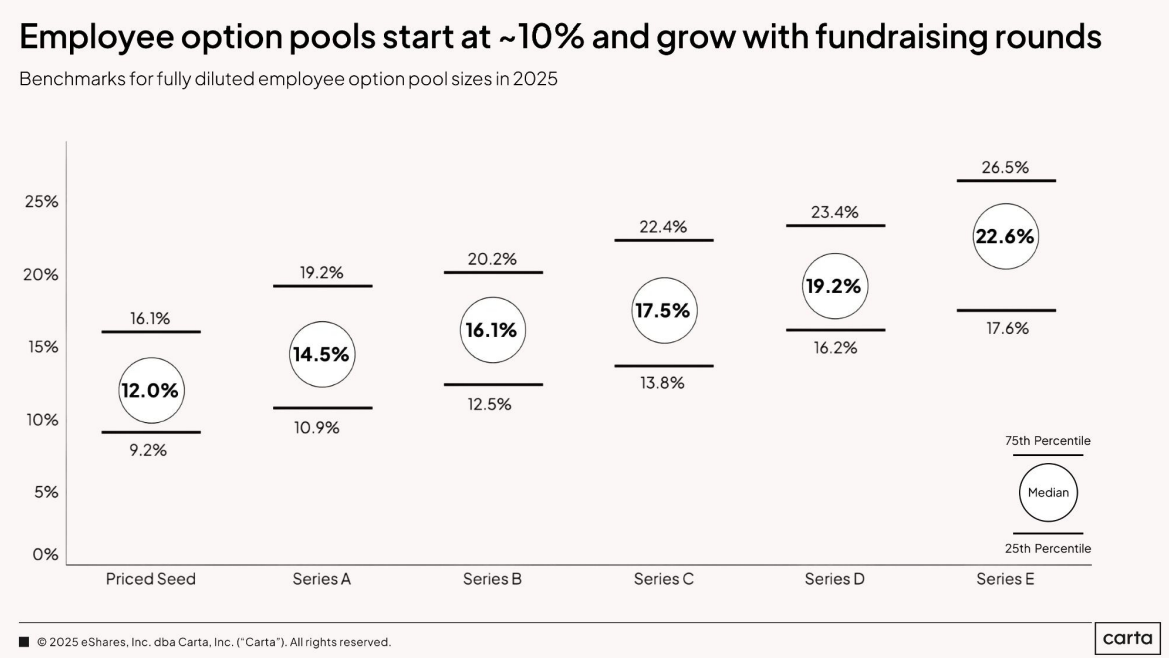

5. Equity Pools to attract the best are on the rise

Equity pools for employees are growing because of the AI talent war, reaching approximately 22% in advanced rounds, such as a Series E.

Even though it becomes more present, it is curious to see that only 30% of employees exercise their options after leaving, which brings me the following reflection:

In the beginning, with the strike price low, exercising options is usually advantageous even in the face of a downround. However, as the company matures, the equity dilutes and the acquisition cost rises.

In these more advanced stages, not every employee has the liquidity to immobilize a considerable share of the family's assets in a private and illiquid asset. While financial risk may seem prohibitive, the potential value left on the table is too high to ignore.

This type of scenario shows that there is a clear opportunity for new liquidity models, such as financing for the exercise of options or microsecondary.

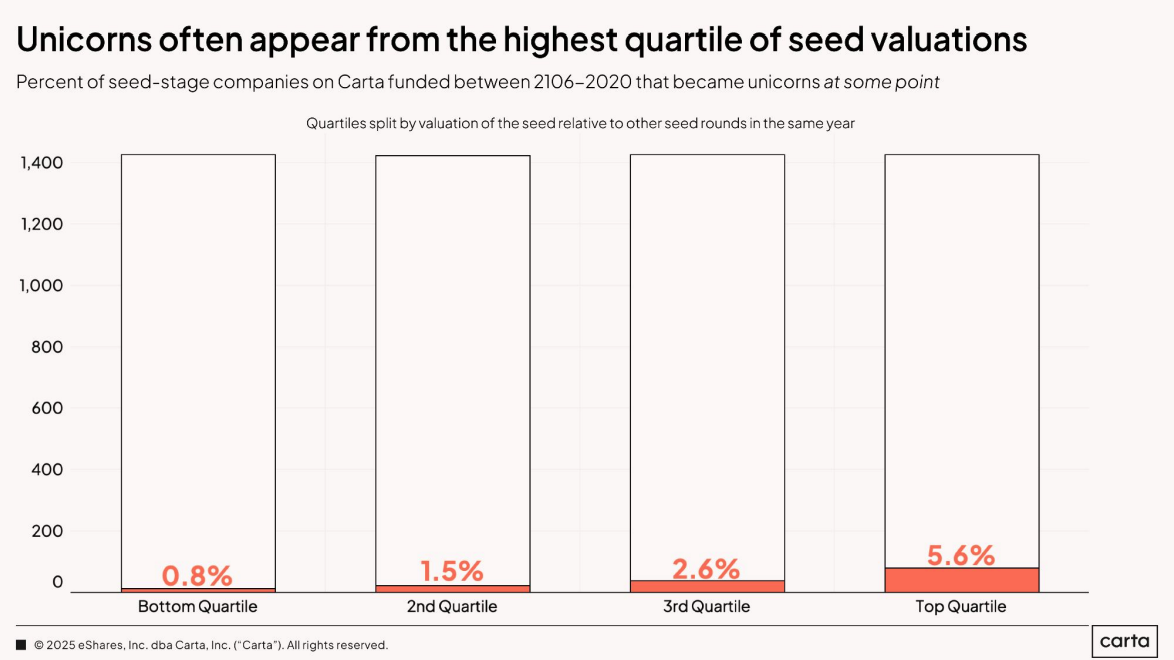

6. Does paying dearly pay off?

In the US, companies in the top quartile of valuation are three times more likely to become unicorns than those in the second quartile. Even so, these first-tier businesses are approximately 5% likely to reach a market value of more than US$ 1 billion.

The fact that more unicorns are leaving the top quartile of valuation seems to me to be more of a correlation than a causation. I affirm this, because the volume of capital raised is the main component of calculating market value - especially in the initial rounds - there is great uncertainty that hangs in the journey of startups that achieve large rounds early on.

On the one hand, companies that attract more are able to accelerate investments in equipment, product, and distribution, which validates the thesis, if the direction is right. On the other hand, high valuations tend to be perpetuated in the following rounds, creating the risk of false positives: companies that grow on paper, but without the corresponding fundamentals.

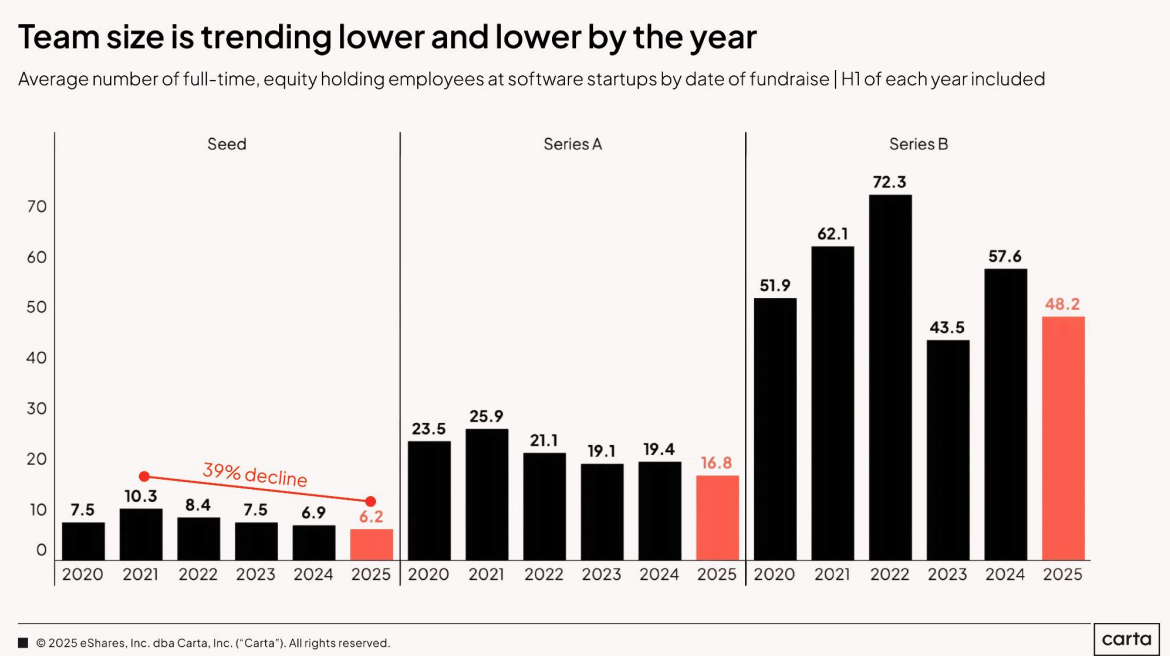

7. People efficiency is absurdly higher in the USA (and has been growing year by year)

In the US, the median of headcount in Seed companies is six employees, while in Series A, it reaches 17. In Brazil, the same indicator, in Seed, is close to 15 to 20 employees, while in Series A, it reaches the level of 40 to 50 people.

It can be argued that traction requirements at Seed differ between countries, but the closer to Series A, the more equalized the rule is. Recent data from an SVB report shows that the median annual revenue of startups in the USA is US$ 2.8 million, a level very in line with our benchmark of Astella Napkin for these stages of the journey.

The conclusion is hard but necessary: to deliver the same revenue result that enables a Series A, Brazilian companies operate with teams two to three times larger. This opens up a productivity problem: we are swelling structures much earlier just to reach the same level of revenue as the North Americans.

In other words, we need to improve this metric a lot. In the last year, we have already seen a clear reduction in this number in newer, AI-native companies, but we are still far from the global benchmark.

This was an in-depth analysis Carta's report, which brings together data from companies in the United States and today represents one of the most complete and qualified bases in the market. Even though we don't have anything equivalent in terms of depth and scope in Brazil, the insights extracted are highly relevant and applicable to our context. After all, the game is global. Here are these findings as important learnings for 2026.